Chart of Accounts Practice Quiz

Chart of Accounts: 20 Practice Questions for Beginners

How well do you know the Chart of Accounts? Let’s find out!

Can you answer these 20 multiple-choice questions on the Chart of Accounts? Click here to watch.

Here are twenty multiple-choice questions on the Chart of Accounts. Can you answer them all correctly? Grab your pen, play along and remember to share your score at the end.

In Financial Accounting, what is an "Account"?

a) A password-protected login for accessing accounting software

b) A list of customers and their contact details

c) A log used only to record bank balances

d) A record that summarizes changes in a specific financial item

A Chart of Accounts is an organized ______ of every account held in a General Ledger. Can you fill in the blank?

a) Directory

b) Catalogue

c) List

d) Statement

Which of the following would not appear in a Chart of Accounts?

a) Cash

b) Accounts Receivable

c) Income Tax Payable

d) Customer Contact Information

The Chart of Accounts groups accounts by ______. Can you fill in the blank?

a) Type

b) Department

c) Payroll cycle

d) Transaction date

In most systems, each account in the Chart of Accounts has a ______. Can you fill in the blank?

a) Reporting segment

b) Unique account number

c) Cost centre

d) Functional area

Why do many businesses use account numbers instead of just account names?

a) To simplify sorting, searching and reporting

b) Because accounting standards require account numbers

c) To hide sensitive account information

d) To prevent accounts from being modified

Which statement is true about customizing a Chart of Accounts?

a) It must follow a fixed global numbering standard

b) It can be customized to suit the business’s reporting needs

c) It can only be updated at year-end

d) It must match the bank statement layout exactly

Why might a business choose to increase granularity in its Chart of Accounts?

a) To reduce the number of Journal Entries required

b) To simplify the Chart of Accounts by removing categories

c) To gain more detailed financial insights for better reporting

d) Because the number of employees increases

How are account categories typically arranged in a Chart of Accounts?

a) Assets → Liabilities → Equity → Revenue → Expenses

b) Revenue → Expenses → Assets → Liabilities → Equity

c) Liabilities → Assets → Revenue → Expenses → Equity

d) Equity → Assets → Revenue → Liabilities → Expenses

Which of these is a type of Asset?

a) Sales Revenue

b) Accounts Receivable

c) Retained Earnings

d) Owner’s Drawings

Which of these is a Liability account?

a) Inventory

b) Bank Loan Payable

c) Wage Expenses

d) Interest Expenses

Which of the following accounts would typically be grouped under Equity?

a) Retained Earnings

b) Prepaid Insurance

c) Goodwill

d) Cash

Which of these is not a Revenue account?

a) Service Revenue

b) Interest Income

c) Sales Revenue

d) Accrued Revenue

Which of these is not an Expense account?

a) Cost of Goods Sold

b) Depreciation Expenses

c) Prepaid Expenses

d) Utility Expenses

Why would a business create sub-accounts?

a) To reduce the number of accounts

b) To comply with government-mandated account structures

c) To provide more detailed reporting under a main category

d) To hide transactions from the general ledger

Which of the following is not a Contra-Account?

a) Accumulated Depreciation

b) Sales Returns

c) Allowance for Doubtful Accounts

d) Accounts Receivable

Which of the following is an example of a Control Account?

a) Cost of Services

b) Sales Revenue

c) Accounts Payable

d) Rent Expenses

Which type of account is a Service business least likely to include in its Chart of Accounts?

a) Service Revenue

b) Accounts Receivable

c) Work-in-Progress

d) Wage Expenses

Which account would you expect to find in a Retail business?

a) Cost of Goods Sold

b) Work-in-Progress

c) Raw Materials

d) Manufacturing Overhead

Which account would you expect to find in a Manufacturing business?

a) Consulting Revenue

b) Finished Goods

c) Unrestricted Funds

d) Membership Fees

Bonus Question! Which account would you expect to find in a Non-Profit organisation?

a) Share Capital

b) Retained Earnings

c) Net Assets Without Donor Restrictions

d) Additional Paid-In Capital

Scroll down to see the answers.

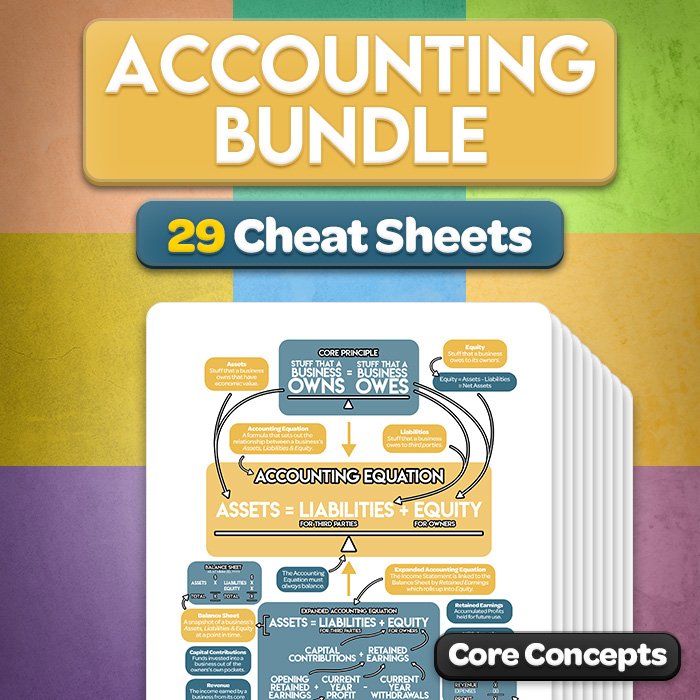

All-in-One Accounting Cheat Sheet Bundle

Get the latest edition of my best-selling Accounting Cheat Sheets. This bundle is perfect for students, bookkeepers and small business owners who want to learn accounting quickly.

Get the latest edition of my best-selling Accounting Cheat Sheets in one powerful, money-saving bundle. Now updated in full color with improved layouts, reorganized sections and brand-new topics requested by learners.

Perfect for accounting students, bookkeepers, small business owners and independent learners, these one-page visual guides make complex accounting concepts easier to understand, review and remember.

Created by James, a qualified accountant and the creator of Accounting Stuff, an accounting education channel with over one million subscribers on YouTube.

What's Included

29 individual, one-page Accounting Cheat Sheets

Clear definitions, useful formulas and visual diagrams

Crisp, color-coded sections for faster learning and better recall

Revised explanations shaped by feedback from thousands of learners

Start Here guide with study tips, a suggested learning pathway and Progress Tracker

30 printable PDFs delivered in one ZIP file

Instant access via email after purchase

Bundle & Save

Buy all 29 cheat sheets together for $39.99 and save $75.72 compared with purchasing them individually. You’ll also receive the Start Here guide and Progress Tracker at no additional cost.

Topics covered

Accounting Foundations

Accounting Equation, Debits and Credits, Bookkeeping Basics, T-Accounts and Journal EntriesThe Accounting System

Accounting Cycle, Chart of Accounts, General Ledger and Trial BalanceAccounting Methods and Adjustments

Cash vs Accrual Methods, Adjusting Entries and DepreciationFinancial Statements

Income Statement, Balance Sheet, Cash Flow Statement (Direct Method), Cash Flow Statement (Indirect Method) and Closing EntriesFinancial Analysis

Financial Ratios, Profitability Ratios, Liquidity Ratios, Efficiency Ratios, Leverage Ratios and Price RatiosInventory

Inventory and Cost of Goods Sold, Inventory Systems (Periodic vs Perpetual) and Inventory Cost Flow AssumptionsAdditional Topics

Bank Reconciliation, Tax Basics and Tax Brackets

How to Use

Work through the cheat sheets in the suggested learning order or focus on the individual topics you want to review. Use them alongside my Accounting Stuff videos, keep them open as an on-screen reference or print the pages you need for your study notes.

Each cheat sheet is supplied as a separate PDF, making it easy to find, download and print only the topics you need.

Please Note

This is a digital product supplied as a ZIP file. No physical item will be shipped.

For personal use by the original purchaser only. Files may not be shared, copied, resold or distributed.

Copyright © 2026 Accounting Stuff Pty Ltd.

All prices are in USD.

Chart of Accounts Quiz: Answers

Here are the answers:

d) A record that summarizes changes in a specific financial item. An Account is a place where a business records, sorts & stores all transactions that affect a related group of items.

c) List. The Chart of Accounts is a list that provides a structure for recording transactions and preparing Financial Statements.

d) Customer Contact Information is not a financial account, so it doesn't appear in the Chart of Accounts.

a) Type. Accounts are usually grouped by category.

b) Unique account number. Account numbers are assigned in ranges based on account category.

a) To simplify sorting, searching and reporting. Account Names can be inconsistent, but numbers keep everything structured and easy to reference.

b) It can be customized to suit the business’s reporting needs. The Chart of Accounts is flexible and can be tailored to suit the needs of different businesses.

c) To gain more detailed financial insights for better reporting. Increasing granularity adds more detail to the Chart of Accounts. This helps a business track specific financial activity.

a) Assets → Liabilities → Equity → Revenue → Expenses. The order follows the Accounting Equation: Assets = Liabilities + Equity. Revenue and Expenses flow into Equity, so they appear after it in the Chart of Accounts.

b) Accounts Receivable represents money owed to the business by its customers. It’s an Asset because it provides a future economic benefit.

b) Bank Loans Payable represent money the business owes to a lender. It’s a Liability because there’s an obligation to make an economic sacrifice in the future.

a) Retained Earnings are a business’s accumulated profits held for future use. It’s an Equity account because it belongs to the owners and increases their claim on the business.

d) Accrued Revenue is a type of Asset. It represents revenue that's been earned but not yet billed or collected.

c) Prepaid Expenses are also Assets. They represent payments made in advance for products or services that will be received in the future.

c) To provide more detailed reporting under a main category. A sub-account is a smaller, more specific account that sits under a parent account in the Chart of Accounts.

d) Sales Returns. A Contra-Account flows against another account and reduces its balance.

c) Accounts Payable. A Control Account summarizes the total balance of a group of related, detailed accounts in a subledger. Accounts Payable summarizes supplier balances.

c) Work-in-Progress. Service businesses don’t produce physical goods, so they don’t use a Work-in-Progress account.

a) Cost of Goods Sold. Retail businesses buy and resell finished goods, so they use Cost of Goods Sold on the Income Statement.

b) Finished Goods. Manufacturing businesses produce physical goods, so they use Finished Goods to record inventory that is completed and ready to be sold to customers.

c) Net Assets Without Donor Restrictions. Non-Profits don’t have owners or shareholders, so they don’t use normal equity accounts. The could use Net Assets Without Donor Restrictions to represent resources available for general use.

How did you score? Let us know in the comments below.

Chart of Accounts: Video Tutorial

The Chart of Accounts (COA) is an organized list of every account held in a General Ledger. You can think of it as an index that categorizes a business's financial transactions into different accounts. In this video, I’ll break down what it is, why it matters, and show you how it looks in Service, Retail and Manufacturing businesses with three simple examples.

In this short tutorial, I attempt to explain how the Chart of Accounts works in less than two minutes!