Journal Entries Practice Quiz

Journal Entries: 20 Practice Questions for Beginners

So, you think you know Journal Entries? Let’s put your knowledge to the test!

In this video I’ll test your understanding of Journal Entries with 20 multiple-choice questions. Can you get them all right?

Can you answer these twenty questions on Journal Entries? Grab a pen, play along and remember to drop your score in the comments at the end!

A Journal Entry is a _____. Can you fill in the blank?

a) Record of a Financial Transaction

b) Type of Financial Statement

c) List of account balances

d) Summary of cash transactions

A Journal Number is a ______ reference number used to identify a Journal Entry. Can you fill in the blank?

a) Random

b) Temporary

c) Optional

d) Unique

The ______ is the date the Journal Entry is recorded in the General Ledger. Can you fill in the blank?

a) Transaction date

b) Entry date

c) Approval date

d) Posting date

Why should every Journal Entry include a description?

a) To meet tax reporting requirements

b) To help users understand the purpose of the transaction

c) To help generate a Trial Balance

d) To post the entry to the General Ledger

Every Journal Entry includes ______. Can you fill in the blank?

a) Only one credit

b) Only one debit

c) At least one debit and one credit

d) Three or more debits and credits

What is a common risk associated with Manual Journal Entries?

a) They're processed too quickly

b) They can bypass normal system controls

c) They automatically balance

d) They can’t be audited

In modern accounting software, Automatic Journal Entries are often created ______. Can you fill in the blank?

a) For one-off or unusual transactions

b) When the Trial Balance is generated

c) When a transaction is recorded through a subledger

d) When Financial Statements are exported

A Simple Journal Entry involves _____. Can you fill in the blank?

a) Three or more accounts

b) Only one account

c) Exactly two accounts

d) No accounts at all

When a transaction impacts three or more accounts, it's recorded as a ______. Can you fill in the blank?

a) Correcting Entry

b) Closing Entry

c) Adjusting Entry

d) Compound Entry

Which of the following transactions would not require an Adjusting Entry?

a) Recording depreciation on equipment

b) Paying a supplier in cash

c) Recording unbilled revenue

d) Accruing unpaid wages

Which of the following errors would not require a Correcting Entry?

a) Failing to record a transaction at all

b) Recording an expense in the wrong account

c) Recording a debit as a credit

d) Misstating an account balance by $50

The main purpose of a Reversing Entry is to ______. Can you fill in the blank?

a) Avoid double-counting revenues or expenses

b) Correct prior-period errors

c) Record depreciation automatically

d) Close Temporary Accounts

Once all Closing Entries have been posted, which accounts still have balances?

a) Temporary accounts

b) All accounts

c) Revenue and expense accounts

d) Permanent accounts

A business issues Common Stock for Cash. What is the Journal Entry?

a) Debit Common Stock, Credit Cash

b) Debit Cash, Credit Retained Earnings

c) Debit Cash, Credit Common Stock

d) Debit Revenue, Credit Cash

A business receives cash from a customer to settle an outstanding account. What is the Journal Entry?

a) Debit Accounts Receivable, Credit Cash

b) Debit Cash, Credit Accounts Receivable

c) Debit Cash, Credit Revenue

d) Debit Accounts Payable, Credit Cash

A business closes its Revenue account at year-end. What is the Journal Entry?

a) Debit Income Summary, Credit Revenue

b) Debit Revenue, Credit Income Summary

c) Debit Income Summary, Credit Expenses

d) Debit Retained Earnings, Credit Revenue

A business records depreciation on its Equipment. What is the Journal Entry?

a) Debit Depreciation Expense, Credit Accumulated Depreciation

b) Debit Equipment, Credit Depreciation Expense

c) Debit Accumulated Depreciation, Credit Equipment

d) Debit Depreciation Expense, Credit Cash

A customer pays in advance for a 12-month subscription. What is the initial Journal Entry?

a) Debit Unearned Revenue, Credit Cash

b) Debit Service Revenue, Credit Cash

c) Debit Accounts Receivable, Credit Revenue

d) Debit Cash, Credit Unearned Revenue

A business buys equipment. It pays part in cash and the rest on credit. What is the Journal Entry?

a) Debit Expenses, Credit Cash, Credit Accounts Payable

b) Debit Cash, Credit Equipment, Credit Accounts Payable

c) Debit Equipment, Debit Accounts Receivable, Credit Cash

d) Debit Equipment, Credit Cash, Credit Accounts Payable

A business mistakenly records a payment for Office Supplies as a Marketing Expense. What is the Journal Entry?

a) Debit Marketing Expenses, Credit Office Supplies

b) Debit Office Supplies, Credit Cash

c) Debit Office Supplies, Credit Marketing Expenses

d) Debit Marketing Expenses, Credit Cash

Bonus Question! A business forgets to accrue Utility Expenses. What is the effect on the Accounting Equation?

a) Liabilities understated, Equity overstated

b) Assets overstated, Liabilities understated

c) Assets understated, Liabilities overstated

d) Liabilities overstated, Equity understated

Scroll down to see the answers.

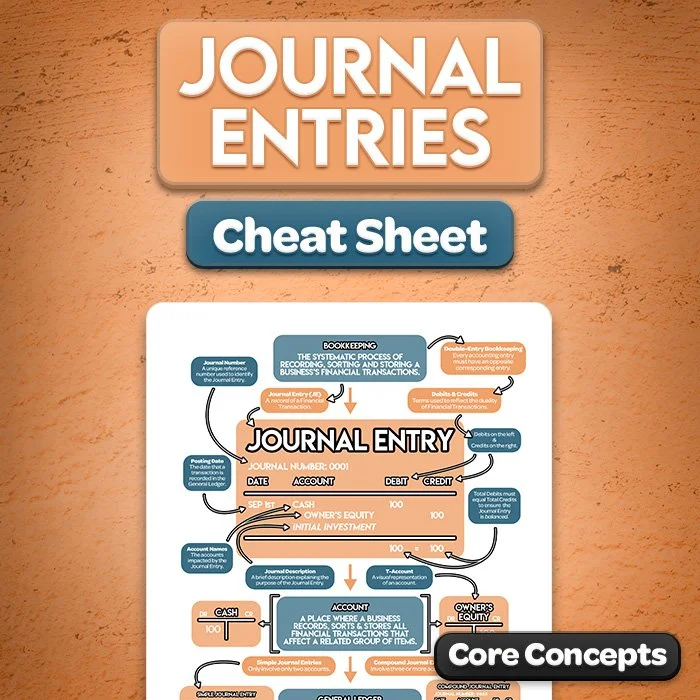

Journal Entries Cheat Sheet

My Journal Entry Cheat Sheet is gives you with a one-page summary of everything you need to know about Journal Entries in accounting. You can download it here.

Build your understanding of Journal Entries with this clear, beginner-friendly cheat sheet. This one-page visual guide brings the key concepts together in one convenient reference that you can view on screen, print, annotate or add to your study notes.

It also summarizes the key information from my Journal Entries video, making it ideal for reviewing the topic after watching.

What's Included

One-page Journal Entries Cheat Sheet

Clear definitions, examples and visual explanations

PDF for on-screen viewing or printing

Instant access via email after purchase

Topics Covered

What a Journal Entry is and how it records a transaction

The key components of a Journal Entry

How Debits and Credits follow Double-Entry Accounting

The difference between Simple and Compound Journal Entries

How Journal Entries flow into the General Ledger and Financial Statements

Please Note

This is a digital product. No physical item will be shipped. The PDF is not interactive, editable or fillable.

For personal use by the original purchaser only. The file may not be shared, copied, resold or distributed.

Copyright © 2026 Accounting Stuff Pty Ltd.

All prices are in USD.

Journal Entries Quiz: Answers

Here are the answers:

a) Record of a Financial Transaction. A Journal Entry is a record of a transaction in an Accounting System.

d) Unique. Journal Numbers are unique reference numbers that help us track and identify transactions.

d) Posting date. The Posting Date determines when a Journal Entry affects account balances.

b) To help users understand the purpose of the transaction. Journal descriptions provide context and improve the audit trail by explaining why the journal was posted.

c) At least one debit and one credit. In Double-Entry Accounting, every Journal Entry affects at least two accounts.

b) They can bypass normal system controls. Manual Entries can skip some of the automated checks so they're prone to errors.

c) When a transaction is recorded through a subledger. Automatic Journal Entries are generated by an accounting system whenever a transaction flows through a subledger.

c) Exactly two accounts. Simple Journal Entries only involve two accounts.

d) Compound Entry. Compound Journal Entries involve three or more accounts. But they still have to balance.

b) Paying a supplier in cash. Paying a supplier is a regular cash transaction that's recorded at the time it occurs.

a) Failing to record a transaction at all. If a transaction hasn't been recorded, we don't correct it. We record it for the first time with a normal Journal Entry.

a) Avoid double-counting revenues or expenses. Reversing entries are made at the start of a new accounting period to cancel out Adjusting Entries from the previous period.

d) Permanent accounts. Closing Entries reset Temporary Accounts to zero. Only Permanent Accounts carry their balances forward to the next accounting period.

c) Debit Cash, Credit Common Stock. We debit Cash to record the cash inflow, which increases Assets on the Balance Sheet. And we credit Common Stock to record the new shares which increases Equity on the Balance Sheet.

b) Debit Cash, Credit Accounts Receivable. When a customer pays off their outstanding balance, we debit Cash to increase it and credit Accounts Receivable to reduce the amount owed. This transaction converts one Asset (Accounts Receivable) into another Asset (Cash). So Total Assets stay the same.

b) Debit Revenue, Credit Income Summary. Revenue is a Normal Credit Account, so we debit it to bring it to zero, and we credit the Income Summary account. This helps us calculate Net Profit for the period in the Income Summary account, before closing it to Retained Earnings in the Balance Sheet.

a) Debit Depreciation Expense, Credit Accumulated Depreciation. Depreciation recognizes the use or wear and tear of a Fixed Asset over time. We debit Depreciation Expenses to record the allocated cost on the Income Statement. And we credit Accumulated Depreciation (a Contra-Asset) to reduce the Equipment's Book Value on the Balance Sheet.

d) Debit Cash, Credit Unearned Revenue. When a customer pays for a subscription in advance, the business receives cash now but it hasn’t earned the revenue yet. So we debit Cash to increase it, and credit Unearned or Deferred Revenue to record a Liability on the Balance Sheet.

d) Debit Equipment, Credit Cash, Credit Accounts Payable. This is a Compound Journal Entry because it affects three accounts. On the one hand, we debit Equipment to increase Assets on the Balance Sheet. And on the other hand, we credit Cash to decrease it, and we credit Accounts Payable which increases Liabilities for the amount still owed.

c) Debit Office Supplies, Credit Marketing Expenses. This error has overstated Marketing Expenses and understated Office Supplies. To fix it, we debit Office Supplies to record the cost in the correct account and credit Marketing Expenses to remove the amount that was incorrectly recorded there.

a) Liabilities understated, Equity overstated. When a business forgets to accrue Utility Expenses, both the expense and the related liability are missing. This means Liabilities are understated because the obligation hasn't been recorded. Expenses are also understated, which makes Net Profit (and therefore Equity) overstated.

How many did you get right? Share your score in the comments.

Journal Entries: Video Tutorial

In this short tutorial, I'll attempt to explain Journal Entries in less than two minutes. We’ll cover Journal Numbers, Posting Dates, Debits and Credits.

In this quick tutorial, I attempt to explain Journal Entries in less than two minutes! Can it be done? Watch to find out.